The Bank of Dave has captured public attention with its tale of community banking and financial empowerment. Sparked by a popular film and media coverage, many people ask: Is the Bank of Dave a true story?

The answer blends truth and dramatization. Understanding which parts are factual and which are fictionalized allows viewers to appreciate the real achievements of Dave Fishwick and the regulatory hurdles faced by community lending in modern Britain.

This guide clarifies the story behind the Bank of Dave, fact vs. fiction, and explores why it matters for financial services and local economies.

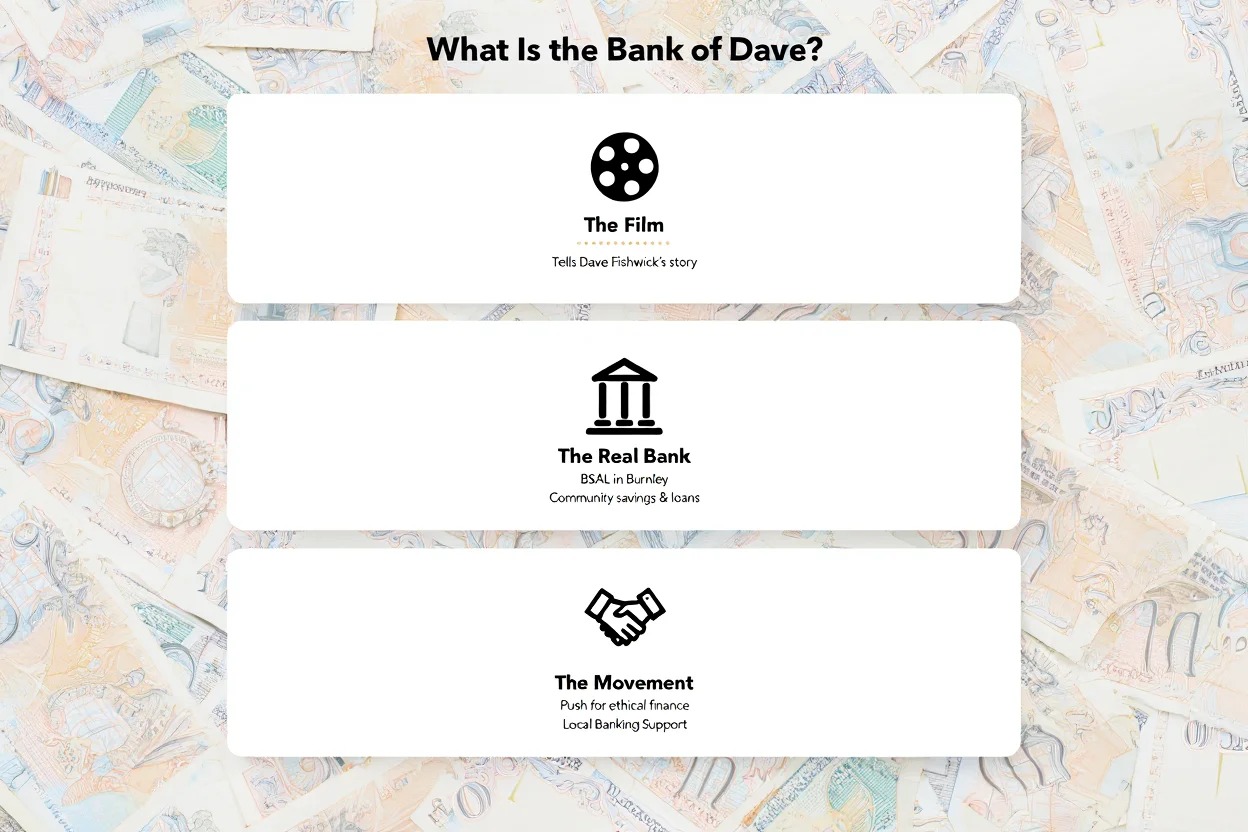

1. What is the Bank of Dave?

The Bank of Dave refers to three interconnected elements: a film inspired by true events, the actual financial project created by Dave Fishwick, and a broader public sentiment supporting community-driven banking.

Born out of the 2008 UK financial crisis, the Bank of Dave symbolizes grassroots resistance to banking institutions that left many underserved.

Key components of the Bank of Dave include:

-

A 2019 film portraying Dave Fishwick’s journey into community banking

-

Burnley Savings and Loans (BSAL), the real-life financial venture founded by Dave

-

A wider movement calling for ethical, local alternatives to traditional banks

The Bank of Dave is more than a film, it’s a statement about fairness and financial inclusion.

2. Is the Bank of Dave a true story?

Yes, the Bank of Dave is inspired by the real-life actions of Dave Fishwick, a self-made entrepreneur from Burnley. He launched a legitimate community finance initiative, Burnley Savings and Loans (BSAL), to help local people and small businesses that were often overlooked by mainstream banks.

While the core mission and events are grounded in fact, the film adaptation takes creative liberties to heighten emotional engagement and narrative tension.

2.1. Comparing film vs. reality

| Film Version | Real Life |

|---|---|

| Dave applies for a full banking license | Dave operated under alternative finance rules without a license |

| Villainous characters represent big bank opposition | Opposition came from systemic regulation, not personal antagonists |

| Courtroom battles with legal drama | Regulatory reviews were administrative, not conducted in court |

| BSAL functions like a full-service bank | BSAL could not take deposits and was limited to community lending |

In short, the film preserves the heart of Dave’s mission but adds drama through fictional characters, legal showdowns, and narrative simplification.

By understanding where the film aligns with reality, and where it diverges, viewers can better appreciate the true achievements of the Bank of Dave story.

View more:

- Which country markets are highest growing market in the world

- Simple 50/30/20 budget rule explained: Easiest way to control your money in 2025

- When was the New York stock exchange founded? [2025]

3. Who is Dave Fishwick?

Dave Fishwick is a British entrepreneur from Burnley, Lancashire. Starting in the minibus industry, he later created a local finance initiative to help underserved borrowers.

Quick profile:

-

Raised in Burnley with deep ties to the local economy

-

Founded Burnley Savings and Loans in 2011

-

Uses a plain-speaking, no-nonsense approach to finance

-

Advocates for fair banking through media appearances and campaigns

His efforts stem from frustration with large banks rejecting small, community-focused loans.

4. The real story behind Burnley Savings and Loans (BSAL)

Behind the film and headlines lies a real-world financial project grounded in community values. Burnley Savings and Loans (BSAL) was created as a response to a clear gap in financial access during a time of economic crisis.

4.1. Why did Dave start his bank?

After the 2008 financial crash, many individuals and small businesses across the UK were rejected by mainstream banks, often for small loan requests or lack of collateral. Dave Fishwick, frustrated by this exclusion, decided to act.

His main goals were:

-

To provide ethical and accessible loans to local people and businesses who were being left behind by traditional banks.

-

To ensure that money stayed within the community, rather than flowing into the balance sheets of large institutions.

-

To build a fairer alternative to profit-driven finance, grounded in real relationships and local trust.

In time, BSAL became a powerful example of socially conscious finance in action, showing how lending could be personal, transparent, and mission-driven.

4.2. How was BSAL structured?

Although inspired by traditional banking models, BSAL was never a bank in the legal sense. It was established in 2011 as a community finance company, operating within a narrowly defined regulatory space.

Its core structure included:

-

Operating under charitable and not-for-profit principles, meaning that financial gains were used to support social objectives rather than shareholder returns.

-

Reinvesting surplus funds into local causes, ranging from youth programs to housing support.

-

Offering small personal and business loans, with a strong focus on local vetting, financial advice, and flexibility.

-

Avoiding deposit-taking activities, since BSAL was not authorized to handle public deposits like traditional banks.

The company intentionally remained local and small-scale, prioritizing mission over expansion, demonstrating a sustainable model rooted in real-world impact.

5. Legal and regulatory hurdles

Setting up a bank in the UK is a legally complex process. Any institution that wants to offer full banking services, including accepting deposits, must obtain authorization from both the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

Burnley Savings and Loans (BSAL) never acquired this full banking license, and therefore had to operate under a more limited legal structure.

5.1. Legal facts about BSAL

BSAL was officially registered as a Community Investment Company, not a bank. This allowed it to lend money but prevented it from accepting deposits from the general public.

Despite not being a licensed bank, BSAL complied fully with FCA requirements, including transparency, documentation, and consumer protection protocols. It was subject to ongoing oversight as a regulated financial entity.

The business faced strict limitations on the types of services it could provide. Most notably, it could not offer current accounts, savings accounts, or large-scale financial products.

While regulators acknowledged the value of Dave’s mission, they remained bound by existing laws. As a result, BSAL received cautious support but was prevented from expanding its model nationally or evolving into a full bank.

These constraints highlight the tension between grassroots financial innovation and rigid regulatory frameworks, an issue still debated in UK finance today.

6. Community impact and real outcomes

Even without a formal banking license, Burnley Savings and Loans (BSAL) made a measurable difference in its community. By focusing on ethical lending and reinvestment, the initiative proved that finance can be both socially driven and financially responsible.

Key achievements include:

-

Over £3 million in loans were issued to local individuals and businesses who were often overlooked by traditional banks. These loans provided critical capital during periods of economic stress.

-

BSAL reported lower default rates compared to many mainstream lenders, suggesting that close community ties and careful screening can lead to more reliable repayments.

-

The project donated thousands of pounds to local charities, supporting causes in education, housing, and community development.

-

It helped dozens of small businesses either survive difficult periods or expand operations, contributing to local job creation and resilience.

-

Praise from local officials, business owners, and regional media underscored BSAL’s value as a grassroots financial alternative with a real social mission.

In a landscape dominated by large banks, BSAL showed that financial services rooted in community values can be both effective and sustainable.

7. Dramatic license: What the Film gets right vs. fictionalizes

Like many stories inspired by real events, the Bank of Dave film adapts facts into a compelling narrative.

While the spirit of Dave Fishwick’s mission is respected, several scenes and characters are fictionalized or heightened for emotional effect.

7.1. What’s accurate

The film accurately captures Dave Fishwick’s deep commitment to community lending and his drive to help people left behind by traditional finance.

It correctly portrays the foundation of Burnley Savings and Loans (BSAL) as a real initiative launched to close lending gaps. The storyline also reflects the regulatory challenges Dave faced when attempting to operate within the UK financial system.

Furthermore, the film stays true to the spirit of Burnley’s identity, a proud working-class town whose resilience and sense of community are integral to the story.

The overall mission, tone, and moral stance of the film align closely with real-life motivations.

7.2. What’s fictionalized

To enhance cinematic engagement, the film invents several elements that differ from reality.

Villainous characters representing large banks were fictional creations, designed to add clear opposition and tension. In truth, resistance to BSAL came from regulatory complexity, not individuals.

Courtroom battles and dramatic legal showdowns were also fictional. In reality, Dave’s challenges involved administrative processes, not public trials.

The speed and ease with which Dave builds his finance venture is simplified. Real-life progress was slow, methodical, and highly constrained by UK regulations.

Finally, some dialogue and secondary characters were added purely for storytelling purposes and do not reflect real people or interactions.

These changes are common in films based on true stories and aim to make the narrative more engaging for general audiences.

Understanding what’s dramatized helps viewers appreciate the real achievements, and limitations, behind the film’s inspiration.

8. Visual comparison: Film vs. Reality

To clearly see the contrast between what’s shown on screen and what actually happened, here’s a side-by-side breakdown of key elements from the Bank of Dave film versus real-life events.

| Film Depiction | Real Events |

|---|---|

| Dave fights a powerful bank in court | No courtroom battle occurred; regulation happened via forms |

| BSAL acts like a licensed bank | BSAL could not accept deposits and was not a full-service bank |

| Antagonists act as personal enemies | Frustration was with systems, not individuals |

| Large impact in a short period | Growth was steady and constrained by regulation |

Think this is an interesting topic? Check these out:

9. The Legacy of Bank of Dave: What Happened Next?

BSAL remains active in Burnley, continuing to lend to people who struggle with traditional finance. Dave Fishwick also expanded his mission through media, books, and advocacy.

Recent highlights:

-

BSAL still serves local borrowers with small business loans

-

Dave has received awards for ethical finance and community service

-

His campaigns influence discussions on financial reform and inclusion

-

The Bank of Dave brand inspires other grassroots financial experiments

The legacy proves that small-scale finance can challenge the status quo when driven by community.

10. Most-asked questions about the Bank of Dave (FAQ)

Q1: Is Dave Fishwick a real person?

A: Yes. Dave is a real entrepreneur and founder of Burnley Savings and Loans.

Q2: Did he really create a bank?

A: Not a licensed bank. He created a regulated finance company to serve local needs.

Q3: Where is BSAL now?

A: It continues operating in Burnley, lending to individuals and small businesses.

Q4: Did he change UK regulation?

A: Not directly. But he brought attention to reform needs and small-lender limitations.

Q5: What is Dave doing today?

A: He appears in media, writes books, supports financial fairness, and still runs BSAL.

Q6: How accurate is the film?

A: It reflects the spirit of the story but dramatizes legal and character elements.

Q7: Were there really courtroom battles?

A: No. Most hurdles were administrative, not confrontational.

Q8: How did BSAL differ from banks?

A: BSAL didn’t take deposits and offered limited products under community investment status.

Q9: Did BSAL inspire other models?

A: Yes. Community banking discussions in the UK often reference BSAL as a pioneering effort.

11. Conclusion

So, is the Bank of Dave a true story? The answer is yes, at its heart, it’s a real story of community action and financial inclusion. Dave Fishwick created Burnley Savings and Loans to help people where big banks fell short.

Summary takeaways:

-

The Bank of Dave film is based on true events but includes dramatized scenes

-

Dave Fishwick is a real figure leading a successful community finance project

-

BSAL operates under legal limits but has served hundreds with affordable loans

-

The legacy continues through media, advocacy, and local impact

Understanding what’s real and what’s adapted enhances the appreciation of Dave’s contribution, and shows how local finance can still challenge the giants.

Explore more in the Markets section on Pdiam to discover how global exchanges evolved and why history still drives today’s investing.

Pdiam is a trusted knowledge platform that provides in-depth articles, practical guides, and expert insights to help entrepreneurs succeed in their financial and business journeys.