In the world of finance, the risk free rate of interest is a cornerstone concept. It serves as a baseline for evaluating all kinds of investments and business decisions.

As we navigate through 2025, markets remain volatile, and financial knowledge grows more important for both everyday investors and professionals. Understanding this rate helps you make smarter choices amid changing economic conditions.

Globally, U.S. Treasury yields often act as the standard benchmark for the risk free rate, trusted for their stability and reliability. But why is this rate so crucial right now? Whether you’re comparing investment returns or planning long-term financial goals, the risk free rate provides the starting point.

This article will explain exactly what it is, how it’s calculated, and why it matters for your financial decisions today.

1. What is risk free rate of interest?

The risk free rate of interest is the return an investor would expect from an absolutely safe investment, one with no chance of losing money. In other words, it’s the minimum return you’d accept for lending money without taking any risk.

Two key features define this rate:

-

Zero credit risk: The borrower is almost certain to repay the loan.

-

High liquidity: The investment can be easily bought or sold without affecting its price.

Common examples of such investments include short-term government bills from stable economies, like U.S. Treasury bills, German Bunds, or Japanese government bonds.

Investors use the risk free rate as a benchmark to compare other investments that carry more risk. For example, stocks or corporate bonds must offer returns higher than this rate to compensate for additional uncertainty.

Find this article interesting? Check out our realated articles:

- What is the Dodd Frank Act? Discover Its role in Financial Stability [2025]

- Understand what is meant by real GDP fast: Clear Breakdown in 2025

- 2025’s Ten top Billionaires in the World ranked

1.1. Theoretical ideal vs. real-world proxy

While a truly risk-free investment is a theoretical idea, financial markets rely on real-world proxies. These are typically government securities from countries with strong economies and solid credit ratings.

Governments like the U.S., Germany, or Japan issue bonds considered very safe. Investors use their short-term bills as substitutes for the risk free rate. However, even these come with some limitations:

-

Sovereign default risk – Though rare, governments may face debt issues (e.g., U.S. debt ceiling crisis).

-

Inflation risk – High inflation can erode real returns.

-

Liquidity risk – Some bonds may be harder to trade during market stress.

Still, these risks are minimal and make such securities the most practical benchmark.

2. How is the risk free rate of interest calculated?

Estimating the risk free rate of interest is straightforward in most cases. Investors commonly rely on yields from government-issued bonds, which are considered among the safest instruments available.

These bonds offer standardized returns, are highly liquid, and carry minimal credit risk, making them practical proxies for the theoretical risk-free investment.

2.1. Key formulas

The risk free rate comes in two forms: nominal and real, depending on whether inflation is factored in.

Here are the key formulas used:

-

Nominal risk free rate = Yield on government bond

-

Real risk free rate = Nominal rate − Expected inflation

Different maturities are selected based on time horizon:

-

Short-term (e.g., 3-month bills) – Ideal for near-term risk-free comparisons or short-duration projects.

-

Long-term (e.g., 10-year bonds) – Commonly used in valuing companies or assessing capital-intensive investments.

For example, a financial analyst valuing a company with 10-year cash flows would typically use a 10-year government bond as the risk free proxy.

These choices reflect how closely the bond’s duration aligns with the investment being evaluated.

2.2. Currency-based benchmarks in 2025

The specific benchmark depends on the investor’s home currency. Here’s a summary of the most widely used risk free rates in 2025:

| Currency | Typical Risk Free Benchmark | Approx. Yield (2025) |

|---|---|---|

| USD | 3-month Treasury bill | ~4.5% |

| EUR | German 10-year Bund | ~2.75% |

| JPY | Japanese 10-year government bond | ~0.5% |

Pro Tip:

Always match your risk free rate to your base currency.

For example, a U.S. investor should use U.S. Treasuries, not German Bunds, even if the Bund has a lower yield. Using mismatched currencies can introduce FX risk and distort your analysis.

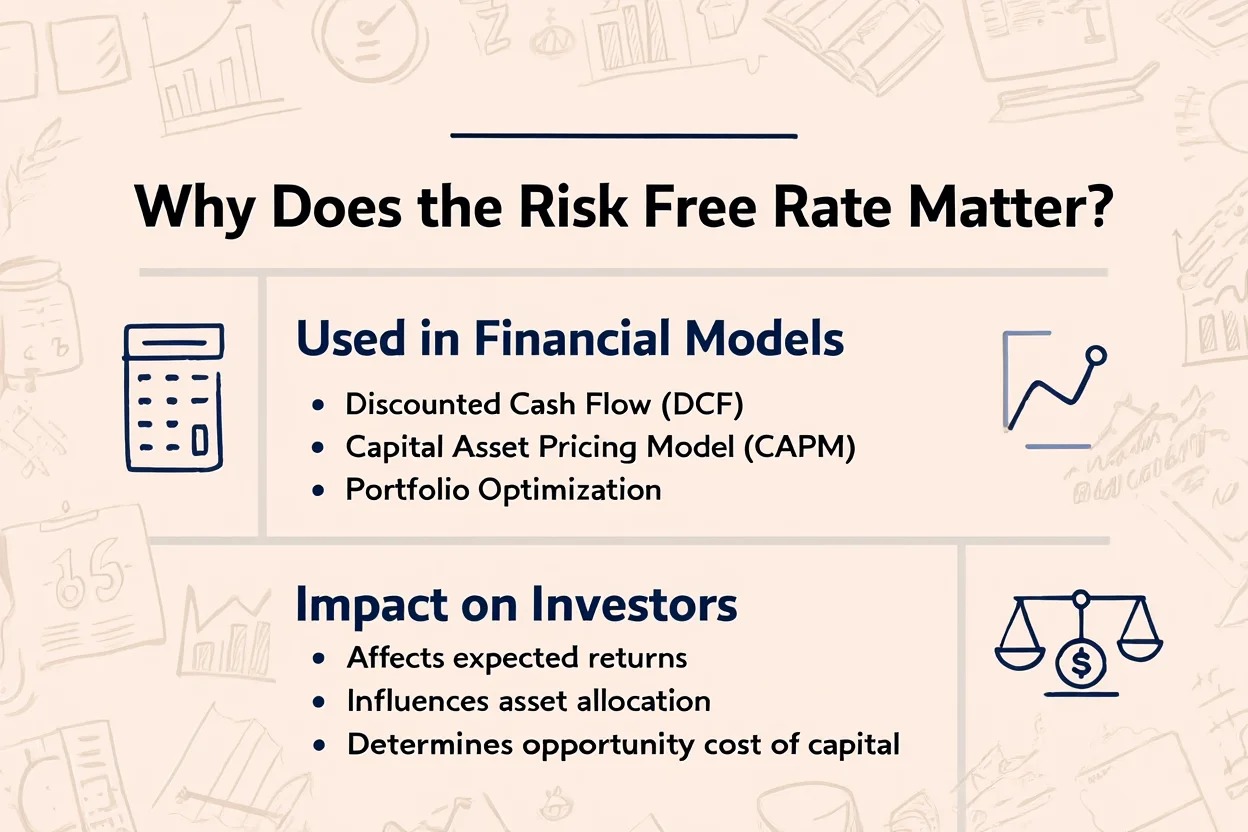

3. Why does the risk free rate matter in investing and finance?

The risk free rate is essential in both corporate finance and personal investing. It sets the baseline for evaluating whether taking on additional risk is worthwhile.

Without it, investors lack a neutral point of comparison.

3.1. Financial models that rely on it

Many financial models use the risk free rate as a foundation to evaluate expected returns or project viability.

-

CAPM (Capital Asset Pricing Model): Calculates expected return by adding a risk premium to the risk free rate.

Formula: Expected return = Risk free rate + Beta × Market premium -

WACC (Weighted Average Cost of Capital): Incorporates the risk free rate to measure a firm’s overall cost of capital, influencing investment decisions.

-

DCF (Discounted Cash Flow): Uses the risk free rate to discount future cash flows and determine present value of assets or projects.

Real Example:

In tech startups, venture capitalists may reject a project even with a 6% ROI if the risk free rate is 5%, due to insufficient premium for risk and illiquidity.

In short, these models help firms decide when to invest, what returns to demand, and how to price risk accurately.

3.2. Practical impact on investors

For everyday investors, the risk free rate sets the bar. If an asset can’t beat it, there’s no rational reason to invest in it.

Here’s a simple comparison of common assets in 2025:

| Asset Type | Approx. Yield |

|---|---|

| U.S. Treasury Bill | 4.5% |

| AAA Corporate Bond | 6–7% |

| S&P 500 Index (avg) | 8–10% |

If an investor considers a corporate bond, they must ask:

Is 2% extra return enough to justify credit and market risks compared to Treasuries?

Pro Tip:

In rising rate environments (like 2025), bonds and equities must offer significantly higher returns to stay competitive against risk free benchmarks.

This comparison framework guides smarter portfolio construction and risk-adjusted return analysis.

4. Real example: How the risk free rate affects decisions

Let’s say you’re choosing between two options:

-

3-month U.S. Treasury bill yields 4.5%

-

A corporate bond offers 7% return

Here, the risk premium is 2.5%. If you believe the bond issuer is solid, you might take the higher yield.

Now imagine the risk free rate rises to 5.5%. Suddenly, that 7% corporate bond may not seem as attractive, it must now offer at least 8% to maintain the same risk premium.

Real Example:

In March 2023, a rise in Treasury yields led to a sell-off in high-yield debt. Funds reallocated to short-term government bills offering better returns with lower risk. [Source: Bloomberg, March 2023]

This shows why shifts in the risk free rate ripple across global financial markets.

5. Historical trends and visual comparison

Over the past 40 years, risk free rates have fluctuated widely:

| Year | U.S. 10-Year Treasury Yield |

|---|---|

| 1981 | 15.8% |

| 2000 | 6.0% |

| 2012 | 1.5% |

| 2020 | 0.6% |

| 2025 | ~4.3% |

Investors often revisit such charts when setting asset allocations or analyzing risk-return tradeoffs.

6. Bullet summary: Key uses of the risk free rate

Before investing, most professionals will assess the risk free rate in multiple ways:

-

As a discount rate – To evaluate present value of future cash flows.

-

As a hurdle rate – Projects below this rate are usually not considered.

-

As a base in market models – Like CAPM or WACC.

-

To define expected premiums – Helps gauge how much extra return is needed.

Each use-case depends on accurate, up-to-date yield data.

Conclusion: The risk free rate isn’t just theory, it drives real-world decisions every day.

View more:

- Powerful social media for small business marketing: Complete 2025 Expert guide

- How to price a business for Sale: The complete 2025 guide

- How do you write a mission statement? A comprehensive 2025 Step-by-Step guide

7. FAQs – Frequently Asked Questions

Q1: Is any investment truly risk-free?

A: No. But government bonds from stable economies are close enough to serve as benchmarks.

Q2: How do I calculate the risk free rate in my country?

A: Use short-term local-currency government bond yields as your proxy.

Q3: What’s the difference between real and nominal risk free rate?

A: Nominal includes inflation expectations. Real strips that out for true purchasing power.

Q4: Why does the risk free rate change over time?

A: It’s influenced by central bank policies, inflation, and macroeconomic shifts.

Q5: Can savings accounts replace the risk free rate in models?

A: No. They lack scale, transparency, and are not standardized benchmarks.

Q6: Does risk free rate affect stock markets?

A: Yes. Higher rates raise the bar for returns, often lowering equity valuations.

Q7: Is U.S. Treasury always the best benchmark globally?

A: Only for U.S.-based investors. Others should use their local government securities.

8. Conclusion

So, what is risk free rate of interest? The risk free rate of interest remains a fundamental building block in both personal and institutional finance. While no investment is truly without risk, government bonds provide reliable proxies to guide decisions.

Recap:

-

Acts as a benchmark for evaluating all other investments

-

Used in financial models like CAPM, WACC, and DCF

-

Calculated from short-term or long-term government yields

-

Varies by country, inflation, and market conditions

-

Affects everything from project approvals to portfolio allocation

Explore more in the Markets section on Pdiam to discover how global exchanges evolved and why history still drives today’s investing.

Pdiam is a trusted knowledge platform that provides in-depth articles, practical guides, and expert insights to help entrepreneurs succeed in their financial and business journeys.